PayPal (PYPL -1.68%) experienced tremendous growth during the pandemic as digital payments exploded in use. However, with increasing competition and shrinking profit margins, investors have been cautious, if not downright pessimistic, about the once-hot payments company.

Since the bull market started in October 2022, the S&P 500 has surged by 44% and the Nasdaq Composite by 74%. Meanwhile, PayPal’s stock has plummeted by 30% and remains 81% below its all-time high.

Under new leadership, PayPal will look to turn things around with its small business offerings and leverage its data trove to scale up its advertising business. With the stock so cheap, is now the time to buy PayPal? Let’s dive into its business plans to find out.

PayPal has struggled with falling margins

With the global digital payment market expected to grow 31% annually through 2030, PayPal’s opportunity is massive. However, the company is undergoing a transition year to improve its margins and get investors excited about the fintech’s growth story again.

In 2021, PayPal forecast it would grow its active accounts to 750 million while doubling its annual revenue to $50 billion by 2025. However, those projections proved excessively optimistic, and the company has since been forced to rethink its business strategy.

Last year, PayPal brought in executive vice president and general manager of Intuit‘s small-business and self-employed group, Alex Chriss, to help turn things around for the fintech company. Chriss’s first task as CEO is to improve PayPal’s offerings for small and medium-sized businesses and reverse the trend in the company’s shrinking profit margins.

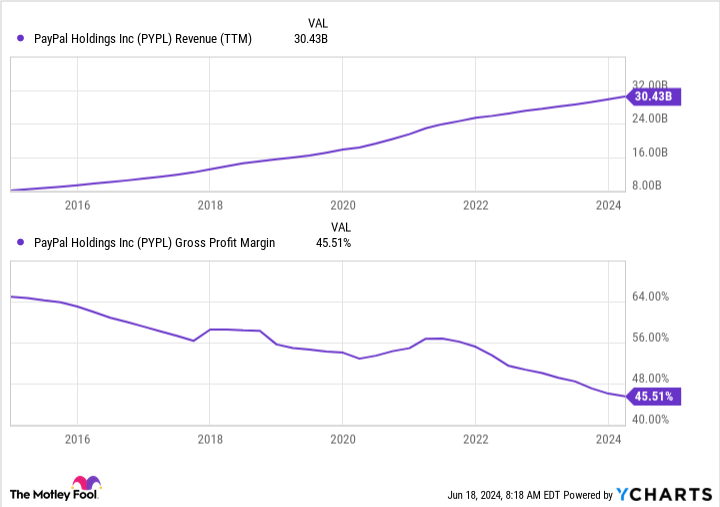

PYPL Revenue (TTM) data by YCharts

Declining margins have weighed on PayPal stock and are a big reason investors are so downbeat about fintech. One cause of this is its falling take rate, which is the percentage of each transaction PayPal retains as revenue after splitting its fees with others. Over the past eight years, PayPal’s take rate has consistently shrunk, falling from 2.89% to 1.76%.

Several culprits are responsible for this. For one, eBay, which owned PayPal until 2015, announced it would not renew its agreement with the company and would turn to Adyen to process payments. At the same time, PayPal’s unbranded checkout options, Braintree and Venmo, experienced excellent growth but came at the cost of a lower take rate.

Here’s how PayPal plans to drive growth

CEO Alex Chriss is taking a multipronged approach to improving PayPal’s underlying business. One of his first tasks is to scale up its PayPal Complete Payments offering. The product targets small and medium-sized companies and allows them to accept PayPal, Venmo, Pay Later (its buy now, pay later offering), credit and debit cards, and digital wallets (Apple Pay and Google Pay).

In the company’s first-quarter earnings call, Chriss noted his “deep passion for helping small businesses succeed” and that “frankly, this is an area where PayPal took its eye off the ball.”

To entice customers, PayPal is laser-focused on helping its merchant customers improve conversion rates. One way it plans to do this is with one-click checkouts, called Fastlane, which it says can reduce checkout times by 40%.

The company is making progress with this offering. In the first quarter, it expanded the platform into Canada, the United Kingdom, and more than 20 European markets. Chriss noted that PayPal has a deeper relationship with customers who use the product, which also reduces churn.

Another area of untapped potential for PayPal is advertising. PayPal has a trove of data on consumer spending and will use that data to help customers discover more products and help merchants sell more effectively. The platform will leverage the company’s data and artificial intelligence (AI) to help merchants provide customers with targeted discounts and personalized promotions.

To help them scale up its ad business, the company recently hired Mark Grether as senior vice president and general manager of PayPal Ads. Grether has worked in the industry for two decades and most recently helped Uber Advertising grow to a $1 billion business.

Buy, sell, or hold PayPal?

PayPal must continue to execute its strategy to entice small and medium-sized companies to its payment platform, and will have its work cut out for it to gain a foothold in the highly competitive digital payment space. It will also take time to build up its advertising platform, but the potential for this platform could be huge, with worldwide retail media ad spending expected to hit $140 billion this year.

With the stock priced at 2.2 times sales and 14.6 times this year’s forecasted earnings, PayPal looks like an excellent value stock to buy today and patiently hold for the next several years.